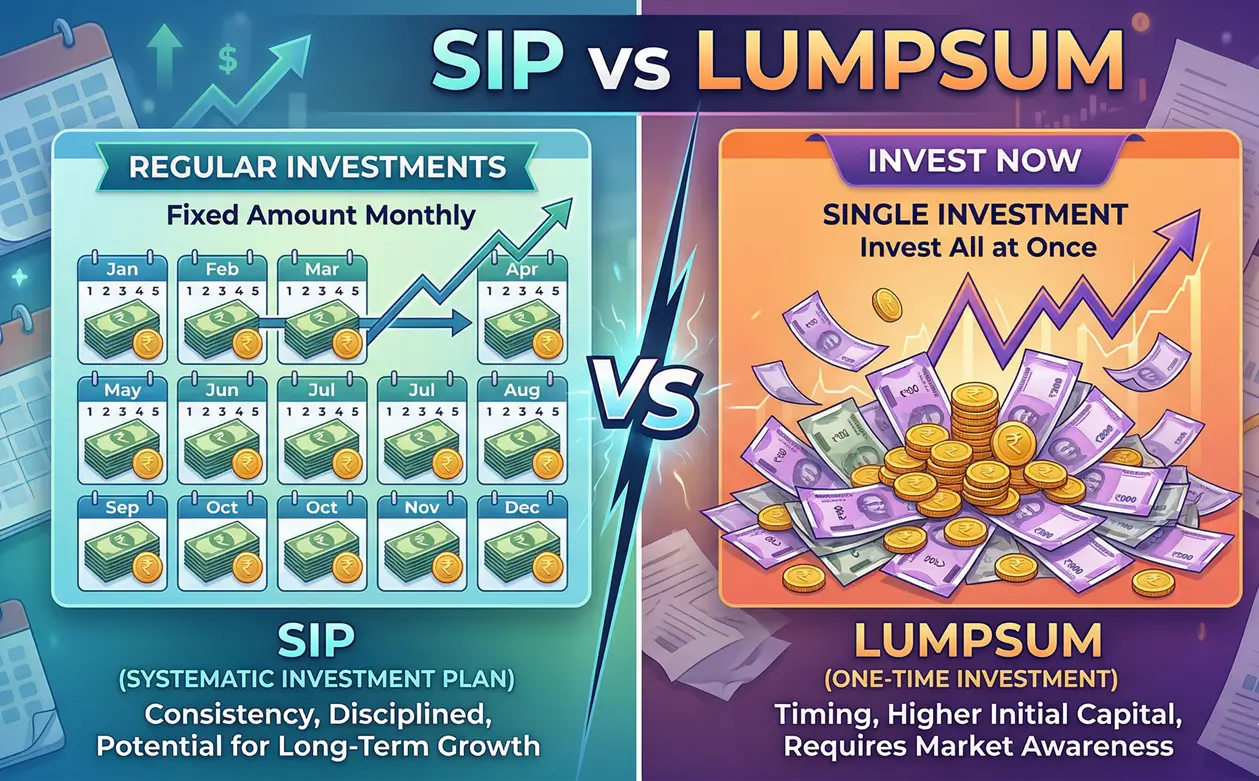

You just got your annual bonus — ₹2 lakh sitting in your savings account. Or maybe you finally set up auto-pay for a monthly ₹5,000 into a mutual fund. Either way, you’ve probably wondered: “Am I doing this right? Would the other approach have made me richer?” This guide settles the SIP vs lump sum debate once and for all — with real Indian market numbers, not theory.

The Question Every Indian Investor Asks

You get a windfall — a bonus, a matured FD, a gift from relatives. Someone tells you to invest it all at once (lump sum). Someone else says spread it out monthly (SIP). Both sound logical. Both have passionate supporters.

Meanwhile, the market is either at an all-time high (so you’re scared to invest the full amount) or crashing (so you’re scared to invest at all). And the money continues sitting in your savings account earning 3.5%.

Here’s the honest answer upfront: both SIP and lump sum can work brilliantly — but they work for different people, different amounts, and different market conditions. The goal of this article is to help you figure out which one is right for you right now.

What is SIP (Systematic Investment Plan)?

A SIP (Systematic Investment Plan) is a method of investing a fixed amount into a mutual fund at regular intervals — typically monthly. Think of it as a standing instruction: ₹5,000 leaves your account on the 5th of every month and buys units in your chosen fund automatically.

How it works in practice:

When the NAV (Net Asset Value — the price of one mutual fund unit) is high, your ₹5,000 buys fewer units. When the NAV is low, your ₹5,000 buys more units. Over time, this averaging effect brings your average cost per unit down — this is called Rupee Cost Averaging, and it is the core advantage of SIP investing.

Example of Rupee Cost Averaging:

| Month | NAV (₹) | Monthly SIP | Units Purchased |

|---|---|---|---|

| Jan | ₹50 | ₹5,000 | 100 units |

| Feb | ₹40 | ₹5,000 | 125 units |

| Mar | ₹30 | ₹5,000 | 167 units |

| Apr | ₹45 | ₹5,000 | 111 units |

| Total | — | ₹20,000 | 503 units |

Average NAV over the period: ₹41.25. But your average cost per unit = ₹20,000 ÷ 503 = ₹39.76. You automatically bought more units when prices were lower — without any effort or market timing on your part.

Key Characteristics of SIP

- Fixed amount invested at fixed intervals (monthly, quarterly)

- Automatic — no emotional decision-making each month

- Rupee cost averaging reduces the impact of market volatility

- Builds the habit of disciplined investing

- Works well for salaried individuals with a steady monthly income

- Can be started with as little as ₹100–₹500/month on most platforms

Use our SIP Calculator to see exactly how much your monthly SIP could grow to over 5, 10, or 20 years.

What is LumpSum Investment?

A lump sum investment means deploying a large amount of money all at once into a mutual fund. You buy all your units at the current NAV on a single day.

Example: You receive a ₹5 lakh bonus in April. Instead of spreading it across 12 months, you invest all ₹5 lakh in a large-cap mutual fund today.

Your entire investment rides the market from day one. If the market goes up from here, your full corpus grows. If it drops, your full corpus takes the hit before recovering.

Key Characteristics of Lump Sum

- Full amount invested at once, at a single NAV

- No averaging — you are betting on today’s price

- Maximum exposure to the market from day one (good and bad)

- Best deployed when markets are undervalued or have corrected significantly

- Works well for windfalls: bonuses, inheritances, matured FDs, property sale proceeds

- Higher potential returns if timed well; higher risk if timed poorly

Use our Lumpsum Calculator to project how a one-time investment could grow over your investment horizon.

SIP vs Lump Sum — The Core Difference Explained Simply

Think of it this way:

SIP = Buying groceries week by week throughout the month. Some weeks tomatoes are expensive (fewer bought), some weeks they’re cheap (more bought). You naturally average your cost.

Lump Sum = Going to the market once and buying everything for the month in one trip. If you went on the right day, great. If you went on a day when prices were high, you paid more than you needed to.

The “right” approach depends on three things: your income structure, your available capital, and the current market condition.

SIP vs Lump Sum — Full Comparison Table

| Parameter | SIP | Lump Sum |

|---|---|---|

| Investment Style | Fixed amount at regular intervals | Full amount at once |

| Rupee Cost Averaging | ✅ Yes — automatic | ❌ No |

| Market Timing Risk | Low — spread across time | High — single entry point |

| Discipline Required | Low (auto-debit handles it) | High (resisting panic/greed) |

| Ideal For | Salaried investors, beginners | Windfalls, experienced investors |

| Returns in Bull Market | Lower than lump sum | Higher — full corpus grows |

| Returns in Bear/Volatile Market | Higher — buys more units at low prices | Lower — full corpus drops first |

| Minimum Amount | ₹100–₹500/month | Typically ₹1,000–₹5,000 one-time |

| Flexibility | Can pause, stop, increase anytime | One-time decision |

| Psychological Comfort | High — no single large commitment | Low — watching full amount fall is stressful |

| Best For | Monthly salary investors | Bonus / windfall investors |

| ELSS Tax Saving | ✅ Efficient (each instalment has 3-yr lock-in from that date) | ✅ Works but full lock-in from investment date |

Real Number Examples — SIP vs Lump Sum in Indian Markets

Let’s run actual scenarios with Indian market context. We’ll use a reasonable long-term equity mutual fund return assumption of 12% per annum (CAGR).

Scenario 1: Monthly Salary Investor — ₹10,000/month SIP for 10 Years

Riya is a 28-year-old software engineer in Pune earning ₹8 LPA. She can invest ₹10,000 per month consistently.

SIP: ₹10,000/month for 10 years @ 12% CAGR

| Total Amount Invested | ₹12,00,000 |

| Estimated Returns @ 12% p.a. | ₹11,61,695 |

| Total Corpus at End of Year 10 | ₹23,23,391 |

Riya turned ₹12 lakh of savings into ₹23+ lakh without ever worrying about market levels.

Run your own monthly SIP projection: SIP Calculator

Scenario 2: Bonus Investor — ₹5 Lakh Lump Sum for 10 Years

Arjun is a 32-year-old sales manager who received a ₹5 lakh annual bonus. He invested it all at once in an equity mutual fund.

Lump Sum: ₹5,00,000 for 10 years @ 12% CAGR

| Amount Invested (One Time) | ₹5,00,000 |

| Estimated Returns @ 12% p.a. | ₹10,52,000 |

| Total Corpus at End of Year 10 | ₹15,52,924 |

Arjun’s ₹5 lakh tripled in 10 years — without any monthly commitment needed.

Check your one-time investment projection: Lumpsum Calculator

Scenario 3: Same Money, Two Methods — The Real Comparison

This is the most revealing scenario. Let’s compare what happens when the same total amount (₹6 lakh) is invested via SIP vs lump sum over 5 years.

Method A — Lump Sum: ₹6,00,000 invested at the start

| Invested | ₹6,00,000 at Year 0 |

| Returns @ 12% CAGR over 5 years | — |

| Total Value after 5 Years | ₹10,57,418 |

Method B — SIP: ₹10,000/month for 60 months (5 years)

| Total Invested | ₹6,00,000 (₹10,000 × 60 months) |

| Returns @ 12% CAGR (SIP basis) | — |

| Total Value after 5 Years | ₹8,16,697 |

In a steadily rising market (12% CAGR), lump sum wins by ~₹2.4 lakh.

Why? Because the lump sum amount is working and compounding from Day 1. The SIP money is still trickling in — the last ₹10,000 invested in Month 60 only has a few days to compound.

But here’s the catch — the real Indian market doesn’t rise smoothly at 12% every year. It crashes 30–40% some years, recovers sharply, and is unpredictable. In a volatile or falling market, the SIP’s rupee cost averaging kicks in and the math flips — SIP investors end up with more units bought at lower prices, outperforming the lump sum investor who put everything in at the top.

The bottom line: Lump sum wins mathematically in a rising market. SIP wins psychologically and practically in a volatile or falling market — which describes most of the Indian market experience.

Scenario 4: The Power of Time — Why Starting Early Beats Everything

Priya starts a SIP of ₹5,000/month at age 25. Rahul starts the same SIP at age 35. Both invest until age 60.

| Priya (starts at 25) | Rahul (starts at 35) | |

|---|---|---|

| SIP per month | ₹5,000 | ₹5,000 |

| Investment period | 35 years | 25 years |

| Total invested | ₹21,00,000 | ₹15,00,000 |

| Corpus @ 12% CAGR | ₹3,24,86,000 | ₹94,88,000 |

Priya invested only ₹6 lakh more than Rahul — but her corpus is ₹2.3 crore larger. That’s the power of compounding doing the heavy lifting over an extra decade.

This is why the best time to start a SIP is always: today. See the impact of starting early vs late with our Cost of Delay Calculator

When Does Lump Sum Beat SIP?

Lump sum outperforms SIP in the following conditions:

1. Markets are significantly undervalued or post a major correction If the Nifty has fallen 25–30% from its peak (like in March 2020 during COVID, or the 2008–09 crisis), deploying a lump sum near the bottom can produce extraordinary returns. The challenge: most investors panic and don’t invest — they wait for “stability” and miss the recovery.

2. You have a long investment horizon (10+ years) Over very long periods (15–20 years), lump sum typically wins in simulations because money gets more time to compound. The starting NAV matters less when you have two decades for the market to grow.

3. You are an experienced investor with strong emotional discipline You can watch your ₹5 lakh become ₹3.5 lakh in a year without selling, because you understand volatility and the long-term nature of equity investing.

When Does SIP Beat Lump Sum?

SIP outperforms lump sum in these scenarios:

1. Markets are at or near all-time highs When valuations are stretched (high P/E ratios, overheated sectors), putting everything in at once risks entering at a peak. SIP spreads this risk across months, giving you multiple entry points — including the eventual correction.

2. You are a salaried investor with monthly income If your money comes in monthly, SIP is simply the most natural and practical approach. You don’t have a large corpus to deploy — you build it gradually.

3. You are a beginner investor The auto-debit nature of SIP removes the most dangerous enemy of investing: your own emotions. You don’t have to decide each month whether “now is a good time.” The system decides for you.

4. The market is volatile and unpredictable (which it almost always is) Rupee cost averaging is most powerful in sideways or choppy markets. When the market yo-yos between 16,000 and 20,000 for 18 months, the SIP investor accumulates units at a low average cost. The lump sum investor who entered at 20,000 is sitting on losses waiting for the market to recover.

The Middle Path: STP (Systematic Transfer Plan)

What if you have a large amount but don’t want to risk putting it all in at once? The answer is STP — Systematic Transfer Plan.

Here’s how it works:

- Park your lump sum (say ₹5 lakh) in a liquid fund or money market fund — low risk, earns ~6–7% p.a.

- Set up an automatic transfer of a fixed amount (say ₹50,000/month) from the liquid fund into your chosen equity mutual fund every month.

- Over 10 months, your full ₹5 lakh moves into equity — but gradually, giving you the averaging benefit of SIP while your money earns returns in the liquid fund during the transition.

STP is the professional investor’s answer to the SIP vs lump sum debate. You get the best of both worlds: your money is always working, and your equity entry is averaged over time.

SIP for Tax Saving — ELSS Funds

If you are using ELSS (Equity Linked Savings Scheme) funds for Section 80C tax deductions, SIP is typically the smarter approach. Here’s why:

In an ELSS fund, every SIP instalment has its own 3-year lock-in period from the date of that instalment. So your January SIP unlocks in January 3 years later, your February SIP unlocks in February, and so on. This means you never have all your money locked simultaneously — some is always unlocking every month after 3 years.

With a lump sum ELSS investment, your entire amount is locked for 3 years from one date. This is less flexible.

Additional benefit: SIP in ELSS also gives you rupee cost averaging within your tax-saving investment, which is a double advantage.

Calculate your ELSS returns and tax savings: ELSS Calculator

Plan your full ₹1.5 lakh 80C allocation: 80C Deduction Planner

Step-Up SIP — The Upgrade Most People Miss

A regular SIP invests the same amount every month for years. A Step-Up SIP (also called a Top-Up SIP) automatically increases your SIP amount every year — typically by 10–15%.

Why does this matter? Your salary grows. Your expenses grow. But most investors keep their SIP amount fixed from Day 1 because changing it feels like effort. Step-Up SIP automates the increase.

The numbers speak for themselves:

| Regular SIP | Step-Up SIP (10% annual increase) | |

|---|---|---|

| Starting SIP | ₹5,000/month | ₹5,000/month |

| Annual increase | ₹0 | 10% each year |

| Duration | 20 years | 20 years |

| Total Invested | ₹12,00,000 | ₹34,36,500 |

| Corpus @ 12% CAGR | ₹49,96,000 | ₹1,00,22,000 |

Step-Up SIP doubles your final corpus compared to a static SIP — simply by keeping up with your rising income.

Learn more about how SIP Step-Up works and whether it suits your investment plan.

Understanding Returns: CAGR vs XIRR

This is where most investors get confused comparing SIP and lump sum returns.

CAGR (Compound Annual Growth Rate) is the right return metric for lump sum investments. It tells you the annual rate at which a single invested amount grew over time.

XIRR (Extended Internal Rate of Return) is the right return metric for SIP investments. Because money is invested at different points in time, CAGR doesn’t work — XIRR accounts for the timing and amount of every instalment and gives you the actual annualised return.

Why this matters: If your SIP statement shows an XIRR of 13%, and your friend’s lump sum CAGR is 14%, these numbers are not directly comparable without understanding the market period and entry points. Always use XIRR when evaluating your SIP performance.

Calculate your mutual fund investment returns: Mutual Fund Returns Calculator 💡 Calculate precise CAGR on your lump sum investments: CAGR Calculator

Which Should YOU Choose? — The Decision Framework

Choose SIP if:

- You earn a monthly salary and want to invest regularly out of it

- You are a first-time investor or have limited experience with equity

- Markets are at or near all-time highs and valuations feel stretched

- You don’t have a large lump sum available — you’re building wealth from income

- You value peace of mind over maximum mathematical return

- You want to build the discipline of goal-based investing for retirement, child’s education, or home purchase

- Your risk appetite is low to moderate

Choose Lump Sum if:

- You have received a windfall — bonus, gratuity, matured FD, inheritance, property sale

- Markets have corrected significantly (15–25%+ fall) from recent highs

- You have a long investment horizon of 10+ years

- You are an experienced investor who can handle short-term NAV drops without panic-selling

- You’ve done your research and are confident in the fund and the valuation

- You want to maximise the power of compounding from day one

Choose STP (Systematic Transfer Plan) if:

- You have a large lump sum but are uncomfortable putting it all in at once

- Markets are at high valuations and you want averaging protection

- You want your money earning returns even while it’s waiting to be transferred to equity

- You are investing ₹3 lakh or more at a time

The Quick Decision Table

| Your Situation | Best Approach |

|---|---|

| Salaried, first-time investor | SIP |

| Got a bonus of ₹1–3 lakh | SIP or STP over 6 months |

| Got a bonus of ₹5 lakh+ | STP into equity over 8–12 months |

| Market fell 25%+ from peak | Lump Sum |

| Market at all-time high | SIP or STP |

| Investing for 15–20 year goal | Either (start now — timing matters less over long periods) |

| ELSS tax saving under Section 80C | SIP (more flexible lock-in) |

Use Our Free Calculators — Run Your Own Numbers

Don’t rely on general examples. Calculate your personal scenario:

- 🧮 SIP Calculator — Project monthly SIP returns over any time period

- 📊 Lumpsum Calculator — See how a one-time investment grows

- 🎯 Goal-Based SIP Calculator — Find out how much monthly SIP you need to reach a specific goal (₹50L for retirement, ₹20L for child’s college, etc.)

- 📈 Mutual Fund Returns Calculator — Compare projected returns across scenarios

- 📉 CAGR Calculator — Calculate the growth rate on your lump sum investments

- ⚡ Power of Compounding Calculator — Visualise what compounding does over 10, 20, 30 years

- ⏰ Cost of Delay Calculator — See exactly how much waiting another year costs you in final corpus

- 🏦 ELSS Calculator — Plan your tax-saving ELSS SIP returns

Pro Tips — Avoid These Common SIP & Lump Sum Mistakes

Mistake 1: Stopping Your SIP When Markets Fall

This is the single costliest mistake SIP investors make. When markets fall, you should be glad your SIP is running — you are buying more units at lower prices. Stopping a SIP during a correction means you miss the units accumulated at the lowest prices, which are the ones that deliver outsized returns during the recovery.

Mistake 2: Waiting for the “Right Time” to Do a Lump Sum

Nobody consistently times the market correctly — not retail investors, not professional fund managers. Studies consistently show that “time in the market” beats “timing the market” over long periods. If you’re waiting for the perfect entry point, use an STP instead of keeping money idle in a savings account.

Mistake 3: Ignoring the Expense Ratio

Whether SIP or lump sum, the fund’s annual expense ratio directly eats into your returns every year. A 1.5% expense ratio vs a 0.5% expense ratio seems small — but over 20 years, it can mean a difference of lakhs in your corpus. Always prefer Direct Plans over Regular Plans for lower expense ratios. Use our Mutual Fund Returns Calculator to compare the impact of different expense ratios.

Mistake 4: Not Accounting for Inflation

A SIP of ₹5,000/month felt significant in 2015. In 2026, ₹5,000 buys noticeably less. If you don’t increase your SIP over time, inflation quietly erodes the real value of your investment effort. Use a Step-Up SIP or manually review your SIP amount annually.

Check how inflation erodes your money over time: Inflation Calculator

Mistake 5: Putting 100% of Investable Surplus Into Equity SIP

SIP and lump sum discussions often assume 100% equity allocation. But your risk appetite, age, and goals matter. A 55-year-old with 5 years to retirement should not deploy all their corpus in equity lump sum — even if markets have corrected. Asset allocation is a prerequisite to the SIP vs lump sum decision.

Mistake 6: Confusing SIP with the Fund Itself

SIP is just the method of investing — it’s not a separate product. You can SIP into a large-cap fund, a mid-cap fund, an index fund, or an ELSS fund. The quality of the underlying mutual fund matters just as much as the investment method.

Helpful Resources on ThriftRupee

Calculators:

- 🧮 SIP Calculator

- 📊 Lumpsum Calculator

- 🎯 Goal-Based SIP Calculator

- 📈 Mutual Fund Returns Calculator

- 📉 CAGR Calculator

- ⚡ Power of Compounding Calculator

- ⏰ Cost of Delay Calculator

- 🏷️ ELSS Calculator

- 💹 Compound Interest Calculator

- 📏 Inflation Calculator

Glossary — Key Terms:

- 📖 What is SIP?

- 📖 What is Rupee Cost Averaging?

- 📖 What is CAGR?

- 📖 What is XIRR?

- 📖 What is ELSS?

- 📖 Lumpsum vs SIP — Explained

- 📖 What is Lumpsum Investment?

- 📖 What is NAV?

- 📖 What is Market Volatility?

- 📖 What is SIP Step-Up?

- 📖 What is Goal-Based Investing?

- 📖 What is Expense Ratio?

Frequently Asked Questions

1. Is SIP better than lump sum for long-term investment in India?

It depends on your situation. For most salaried investors in India who receive income monthly, SIP is the better and more practical choice — it automates investing, removes emotion, and leverages rupee cost averaging. For investors with a large lump sum available (bonus, matured FD, inheritance) and a 10+ year horizon, lump sum can generate higher returns mathematically — especially if invested when markets have corrected. The honest answer: the method matters less than starting early and staying consistent.

2. What is rupee cost averaging and why does it favour SIP?

Rupee cost averaging means that when you invest a fixed amount regularly, you automatically buy more mutual fund units when prices (NAV) are low and fewer when prices are high. Over time, this brings your average purchase cost below the average NAV — which is a mathematical advantage in volatile markets. It’s the core reason why SIP works well even when you can’t predict market direction.

3. If I have ₹5 lakh as a bonus, should I invest all at once or as SIP?

Neither extreme is necessary. The smartest approach is an STP (Systematic Transfer Plan):

- Park ₹5 lakh in a liquid mutual fund (earns ~6–7% and is safe)

- Set an automatic monthly transfer of ₹50,000 into your equity fund

- Over 10 months, your full amount moves to equity — averaged across market levels

This way your money is always working (even in the liquid fund), and your equity entry is averaged. Use our Lumpsum Calculator to compare scenarios.

4. Can I do both SIP and lump sum at the same time?

Absolutely — and many experienced investors do exactly this. You can maintain a monthly SIP from your salary AND deploy a lump sum (or STP) when you receive a windfall. These are not mutually exclusive. In fact, combining both approaches — regular SIP for salary income, lump sum/STP for bonuses — is often the most effective strategy for building long-term wealth.

5. Which is better for ELSS tax saving under Section 80C — SIP or lump sum?

SIP is generally better for ELSS. With ELSS SIP, each monthly instalment has its own 3-year lock-in from that instalment’s date — so after the first 3 years, some portion unlocks every month. With lump sum ELSS, your entire amount is locked for 3 years from a single date, which is less flexible. Additionally, SIP gives you rupee cost averaging within your tax-saving investment. Use our ELSS Calculator and 80C Deduction Planner to plan your tax-saving investments for the year.

6. Does SIP always give lower returns than lump sum?

In a consistently rising market, yes — lump sum mathematically outperforms. But Indian markets are not consistently rising. They are volatile, experiencing regular corrections of 10–30%. In volatile or sideways markets, SIP’s rupee cost averaging advantage means it often matches or beats lump sum returns. The XIRR of a well-maintained 10-year SIP in Indian equity markets has historically been in the 12–15% range for diversified equity funds.

7. What is the minimum amount to start a SIP in India?

You can start a SIP with as little as ₹100/month on some platforms (like Groww, Zerodha, Paytm Money) and most funds accept a minimum of ₹500/month. There is no upper limit. The key is to start — even a ₹500/month SIP compounding for 20 years becomes a meaningful corpus. Use our SIP Calculator to see what any monthly amount grows to over your investment horizon.

Conclusion: The Real Answer to SIP vs Lump Sum

After all the numbers, scenarios, and comparisons, here’s the truth that most articles bury:

The SIP vs lump sum debate is largely a distraction from the more important question: are you investing at all?

A ₹5,000/month SIP started today will beat a ₹10,000/month SIP started three years from now. A lump sum of ₹2 lakh invested today in a good diversified equity fund will beat a “perfectly timed” ₹2 lakh invested when you finally feel confident about markets — because that confidence never comes.

The practical advice:

- If you have a salary → Start a SIP today. Even ₹1,000/month.

- If you have a bonus or windfall → Use STP to move it into equity over 6–12 months.

- If markets have crashed significantly → Consider deploying lump sum. These moments, while scary, are historically the best entry points.

- If you’re unsure → Run the numbers with our calculators, then decide.

The best investment method is the one you’ll actually stick with for 10–20 years. For most Indians, that’s SIP.

Start Planning With the SIP Calculator

Compare Lumpsum vs SIP for Your Amount

Find Your Target SIP With the Goal-Based SIP Calculator

Disclaimer: This article is for informational and educational purposes only. Mutual fund investments are subject to market risk. Past returns are not indicative of future performance. Please consult a SEBI-registered investment adviser before making investment decisions.

Disclaimer: This article is for informational purposes only and does not constitute professional financial or tax advice. Tax laws are subject to amendment. Please consult a qualified Chartered Accountant before making decisions specific to your financial situation.